- July 20, 2019

- Posted by: Tofazzul Hussain

- Category: Business and Investment

A recent business deal has attracted the attention of many. Investors, analysts and all concerned in the business community of Bangladesh are abuzz with this transaction, which has been occurred between Lafarge Surma Cement Limited and the shareholders of Holcim Bangladesh Limited. Lafarge Surma Cement Limited has bought88,244 shares (100 percent) of Holcim Bangladesh Limited against a purchase consideration of $117 million (about Taka 950 crore) most likely under a share sale and purchase agreement executed between the parties. There are several news leads since August 2017 in prominent daily newspapers regarding this transaction. In fact, it deserves attention of the business reporters because Lafarge Surma Cement Limited is a publicly listed company in Bangladesh. And by being a listed company, as per DSE listing rules& regulations, Lafarge Surma is required to publish any significant news or event concerning its business for public information.

Accordingly, Lafarge Surma has informed the public about the news. The transaction as apparently occurred with non-resident foreign shareholders with the demand of the seller to remit the consideration of sold shares to the beneficiary- Amsterdam-based Holderfin BV.The transaction called for approval from the Bangladesh Bank.

The buyer, Lafarge Surma, duly sought the approval through its banker to remit the agreed sale consideration to the beneficiaries in the Netherlands. How much to remit? Taka 106,000 (One lac six thousand Taka) per share!An astronomical price for a share of company. Nevertheless, Bangladesh Bank reviewed the valuation and compared Holcim’sshare price, as reported by newspapers, with that of available similar multinational company listed on our bourse, DSE. The review revealed a humble market price of Taka 450 on that day for a share of the similar company in cement sector. The central bank also compared the share value of Holcim with British American Tobacco Bangladesh Company Ltd (BATBC), whose share is considered the most expensive in the stock market. With a Tk 10 face value, the then market price of each share of BATBC was Tk 2,960.Regardless of the gap between the share prices of Holcim and the control group, the central bank has approved a total payment of 500 crore Taka which is tantamount to Taka 57,203 per share of Holcim.

We have been following the case attentively only to come up with an agape question to know how on earth a company’s share can be so valuable against a face value which is presumably as low as either Taka 10 or 100?Well, it looks okay when we compare the market price of a share of branded company such as Berkshire Hathaway in the USA, and to theobjective valuation of shares of a few remarkable companies traded at the DSE. In latter cases, our simulated valuation of companies operating in Bangladesh through various valuation techniqueseasily find intrinsic value of shares of those companiesfar higher than the quoted price in the market.Mentionable is the experience professionals- financial due diligence reviewer and valuation expert, who come across many instances where buyer (mainly foreign buyers) of a local company considersmany relevant factors ranging from strategic business interest to organizational system and business reputation of the acquired company. In business valuation, those unseen strengths of a company matter most than any other factor. Once Bill Gates happily announced that what readers saw in the balance sheet of his company was perhaps 3 percent of its total economic resources whereas 97 percent was not booked.

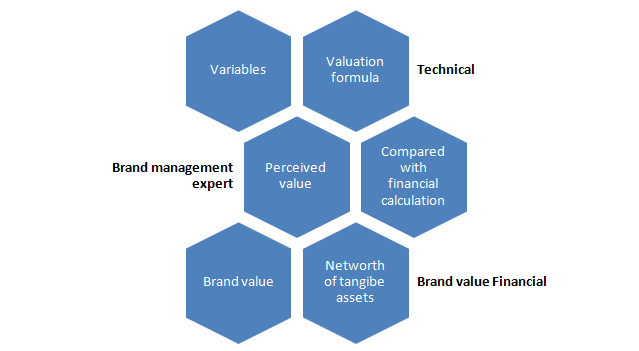

Generally, a business is valued by following a handful of valuation methods.Ideal one includes brand value which is about 70%-90% of the total value of a company, where total value isspeculated, engineered via use of some growth formula, apart from mainstream asset based net worth calculation.

Most commonly used method is the book value method, which we know as net asset value method where financial informationis presented in line with the applicable financial reporting standards (IFRS/BFRS).Whilst book value method is supposed to be an objective valuation with the display of the accumulated wealth of a company, it runs the risk of undervaluation. Therefore comes the market based method to base the company valuation on earnings or EPS. Under market-basedapproach, we compare the NAV with market capitalization of the company (if publicly traded) to indicate the demand of public and to determine how many times of NAV is the market-cap. The wider the gap between market-cap and NAV, more valuable the company is in the eyes of the investors. Other ways under market-basedapproach include EPS times, anddividend yield discounting method. Cash discounting of future earnings based on EPS trend looks smart and perceptive, but it is full of uncertainties and can highly be subjectivegiven the infinite scale we foresee and for the volatility of interest rate over the time horizon. As Warren Buffet rightly says “To properly value a business, you should ideally take all theflows of money that will be distributed between now and judgment day and discount them at an appropriate discount rate.That’s what valuing businesses is all about. Part of the equationis how confident you can be about those cash flows occurring.Some businesses are easier to predict than others”.

Invariably, the valuation result of one method differs with another because these methods are more of judgmental than of scientific.Creativity prevails over objectivity due to the universal law of demand-supply. A share of a company is not foreign to this law of economics.Therefore, we at times find that a company share is available at a price lower than its NAV and sometimes too much above and much beyondthe real worth although the projected EPS/NAV ratio is discouraging.

Warren Buffet, the unquestionable investment guru, who make Benjamin Graham, Philip Fisher, John Burr Williams, and CharlesMungerresponsible for his financial education has framed hisunique investing approach to pick companies instantaneously almost in the blink of an eye.In valuation,Mr Buffett considers a company’s future prospect, the continuing demand of the products of the company, ability of the company to generate revenue against each dollar of investment, the attachment of the products to consumers. EPS growth based multiples i.e., EPS*(PE+EPS growth times 2) is also another favorite valuation technique of Mr Buffett resulting in many cases purchase by him of a company at many times of its NAV.Why the rush? Because of a few but most important buzz words: brand name and its products’ future prospects on that brand, and for fundamental reason that the company’s products are attachedto the mass people and to the development of the nation.

On those bases, a right company can be precious. We have estimated that a company operating for last 50 or 60 years can possibly accumulate a vast wealth for its shareholders provided the company operates in the right sector under the management of a group of right people.Perhaps the discussed share sale and purchase transaction between Lafarge Surma and shareholders of Holcim has been the result of such important considerations.

We appreciate this transaction. This transaction can surely lead us to evaluate objectively whether in the market publicly traded companies are overvalued or undervalued. We can have an indication to revalue the companies. In this regard, it is worth mentioning here that the share transfer by the institutional shareholders of Singer Bangladesh Ltd in recent past in 2017 has been done at market price. Sad enough for general public shareholders of Singer Bangladesh Ltd because they could have gained little more had the share sale and purchase been done at the method adopted by the shareholders of Holcim to transfer its shares to Large Surma. Public shareholder group of Singer Bangladesh Ltd perhaps have been deprived from the potential gain that could have rubbed off to the share price ofSinger for that deal because its intrinsic value was supposed to be much higher than quoted price because Singer is a company of branded products with attachment to consumers’ life since last 40 years. Anyway, our aim is not to delve into that but to highlight key points how to carry out the valuation of a highly regarded company, which is in fashion.

Business world is within social world. Word of mouth matters. It takes time for a company to attach with its customers to find itself valuable provided it serves consumers’ need and its products have utilities. As such, buyers become loyal; demand of its products gets high. As a result, the company is valued at several times of its tangible assets or earnings.Let’s find some of them. Thank you.

About the writerof this Article:

TofazzulHussain FCA, Lead Consultant & Chairman

HUSSAINS Business Consultants Ltd, a business & tax advisory firm

https://today.thefinancialexpress.com.bd/anniversary-issue-2/company-valuation-a-review-1511361586